The emergence of the newspace industry, characterized by the entry of private companies into the space industry, has significantly advanced the development of on-orbit servicing (OOS): any activities carried out upon satellites in orbit by other spacecraft. This progress is largely due to advancements in automation, robotics and navigation technologies that enabled intentional maneuvers to bring a satellite close to another object in orbit for docking or conducting nearby operations. These developments, combined with the miniaturization of components and reduced launch costs, have made OOS more feasible than ever before. However, the level of industry interest and economic viability of such services are subject to several complex dynamics, indicating that bringing OOS to market may be a slow process.

Limited interest in extending the life of LEO satellites

One of the primary motivations for OOS is to extend the operational lifespan of satellites. However, in low Earth orbit (LEO), the low cost of launching satellites has reached a point where the risk and cost of OOS operations do not justify the benefits. It is often more practical and economical to launch new, more advanced satellites rather than prolong the life of existing ones. Furthermore, satellite operators are increasingly enhancing the propulsion capabilities of their satellites, improving autonomy and flexibility, thereby diminishing the need for external support to extend their operational lifespan.

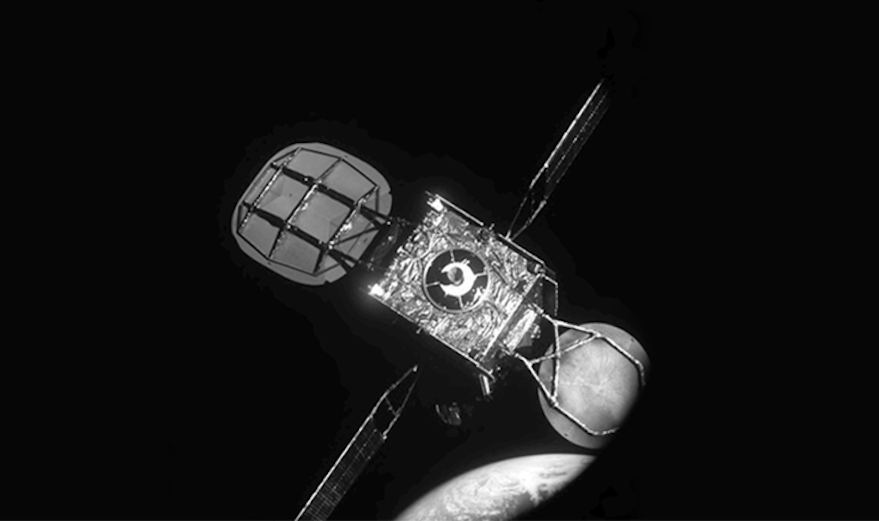

In contrast, extending the life of satellites in geostationary orbit (GEO) offers significant value to operators who face profitability challenges. Northrop Grumman’s Mission Extension Vehicle demonstrated the feasibility and benefit of such services by extending Intelsat 901’s life by five years — a 25% lifespan increase. However, the GEO market is undergoing disruption due to the emergence of broadband megaconstellations in LEO. This shift presents a dilemma for…

Read the full article here

{kind=link}